/_Cropped%20Version/_Cropped%20SVGs/ZayZoon%20Logo-FC-Cropped-Slate%20text.svg)

/_Cropped%20Version/_Cropped%20SVGs/ZayZoon%20Logo-FC-Cropped-white%20text.svg)

| MARCH 19, 2021 |

Shayan Rahnama

Shayan Rahnama

In the United States alone, over $1 trillion is held up in pay cycles as employers give their employees short-term loans for their labor. This has been the norm for far too long now and many businesses don’t realize just HOW big a favor this is.

Shayan Rahnama recently took some time to share his thoughts on Wages On-Demand and its effect on employers and employees. Pulling from his past job experience at FundThrough, an invoice funding platform for businesses, as well as his knowledge from his role as VP of Product at ZayZoon, Shy offers a unique and insightful perspective on cashflow issues from an employer and employee perspective.

Originally a three-part series that can be found on Shy's Linkedin Page, we've combined all the pieces together in one spot for you here to get Shy's point of view on ZayZoon's Wages On-Demand and the earned wage access industry.

It is no surprise that there is a staggeringly large portion of the population in the US that lives paycheck to paycheck - a phenomenon not limited to low income earners. This was true before the pandemic took hold of the economy, and for those who find themselves still earning any income at all, this reality rings even more true today. Almost two thirds of Americans now say they live paycheck to paycheck (roughly 20% more than before the pandemic), and 82% would be unable to afford a $500 emergency expense should it arise.

My previous company provided factoring services for businesses, basically advances on invoices that were coming due or were overdue. There, I felt the visceral reality of cash flow misalignment for business owners. When a supplier’s expenses arise before invoices are paid by buyers, businesses can find themselves in a very tough spot -- especially if buyers pay their invoices late. Often it isn’t the amount of money in and out that is the problem, it’s simply the timing of when cash comes in relative to when cash needs to go out. This can be exacerbated by seasonality, volatility in costs, and industry ups and downs.

Now, working for ZayZoon, which works with employers to offer employees access their wages on-demand, between paychecks, I’m finding that the same is true for those employees. In my early days here, my good friend Karim Gillani (General Partner at Luge Capital, a VC firm focused on FinTech) sent me an awesome NPR podcast that outlined that nearly one third of Americans can’t pay their bills on time (the key factor being the timing, not that they can’t afford the bills). This is exacerbated by “vicious cycle” predatory products like overdraft and payday loans. The podcast positioned payroll as a very short term loan that employees make to their employers. If you get paid monthly then the “loan” you’re making is for 1-30 days, since technically you are accruing hours worked and the amount owed to you is growing from the moment you received your last paycheck to the moment you receive your next. Overall in the US, at any given moment there is over $1 trillion dollars held up in pay cycles.

The most expensive loans out there are short term loans. I saw this at my previous company, where we charged anywhere from 15-40% APR for a 30-90 day loan. This is certainly the case when we look at how expensive payday loans are -- both because these loans are not secured and because they can get away with it. Credit card debt is another example with interest rates around 20% APR. Given how expensive short term loans are for everyone else, the value of the loan you make to your employer (by letting them pay you every 2 weeks or monthly instead of every day) is actually pretty high. If interest were paid out at 20% to a person earning $15/hr or $40,000/yr, on the amount that accrues between paychecks, that person could make an extra $1,350 a year. Not insignificant for an individual, and across all the employees within an organization, this makes up a huge benefit for employers (e.g. at least $135,000 for a 100 employee location at minimum wage).

Employers do not do this out of malice -- delayed payroll cycles were born out of an administrative need imposed by the introduction of Income Tax in World War II. This was designed to raise funds for the war and to curb inflation at wartime, since people were spending less on things they didn’t need. With the need for employers to collect tax came complexities around accounting and withholding money, and showing employees what was deducted and why, and that’s how we ended up with delayed paychecks and paystubs.

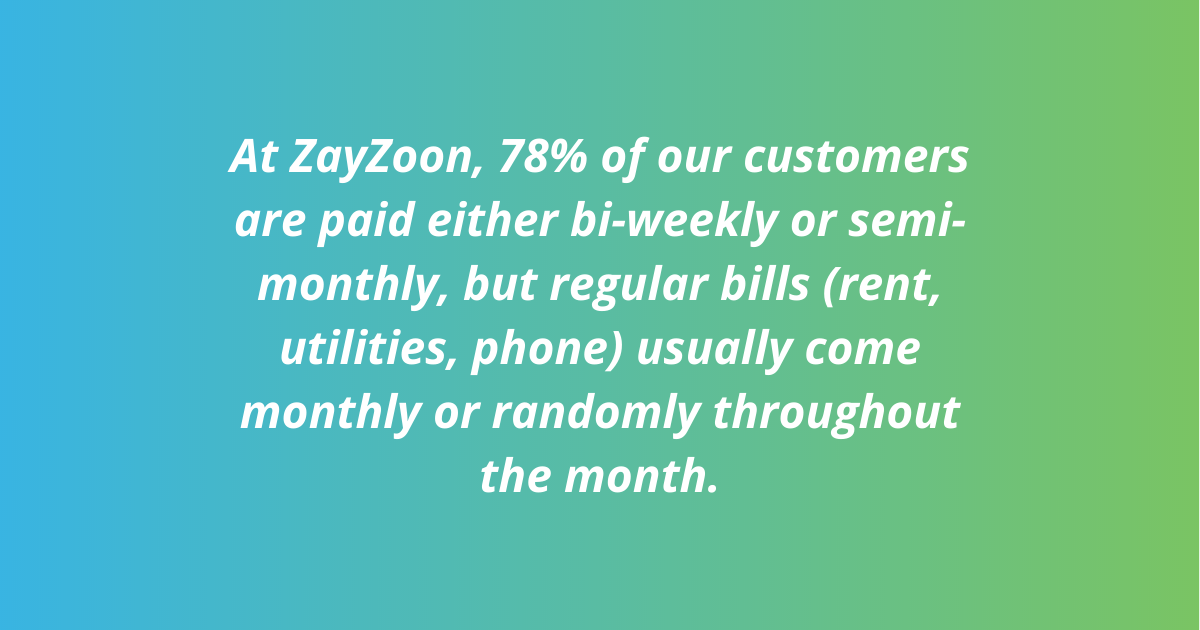

The problem is this doesn’t work for the people getting paid. Like with businesses waiting for invoices, the timing of cash flow in and out is a challenge for the average worker. At ZayZoon, 78% of our customers are paid either bi-weekly or semi-monthly, but regular bills (rent, utilities, phone) usually come monthly or randomly throughout the month. Extraordinary expenses can also arise at any time. This has happened to all of us, and does happen to employees across the income spectrum.

So what can Employers do to help Employees out? Given the immense value Employers get from Employees by deferring wages until payday, what can they do in return?

The single biggest thing employers can do for their employees is to give them access to the wages that they’ve earned between regular paydays, so that they can better align inbound cash flow with the expenses in their lives. This was the case before COVID-19, and it’s especially true during the recession and recovery the pandemic will have led to.

There is a strong need for Earned Wage Access between paychecks, and out of this need has arisen numerous options for employees (including ZayZoon). Some of these are offered through employers, and other options work around the employer, but the employer-offered options are better for employees because:

- They are generally lower cost -- they are integrated with employee payroll and often timesheet systems, and are therefore lower risk and lower cost to the employee

- They are easier - the options that work around employers most often require employees to either pay a large fee, or require employees to enrol for a special card and pay for other services (although many of our competitors require this too)

- They don’t have an arbitrary limit - because services that work around employers aren’t embedded and don’t have as much data, they often limit wage access to amounts that have very little to do with how much an employee worked and earned

In essence, options offered outside of the employer are still payday loans, they’re just tiny ones that can be less predatory because the businesses offering them make money in other ways.

Offering Earned Wage Access as an employer, aside from being better for the employee, has other massive benefits as well. In a survey we conducted earlier this year, we learned a lot about the value that offering Earned Wage Access can bring to employers:

- 89.7% of respondents said that ZayZoon decreased their financial stress.

- 69.8% of respondents said that ZayZoon made them want to pick up more shifts

- 70.7% of respondents ranked early access to wages as extremely important in choosing where to apply for jobs

Needless to say, there is an insane amount of tangible benefit when it comes to improved productivity (through reduced stress), and a huge improvement in being able to attract and retain talent. This is why Earned Wage Access has become a must-have benefit offered by many large retail and fast-food chains, and has become a de-facto standard in a number of industries like quick-serve, home care, gig services, and retail.

For employers in both these industries and others, having a strong, tangible Financial Benefit can be a no-cost or low-cost way to add value for employees in a very impactful way. I’ll be honest, that’s the gist of our pitch to clients, and the heart of the sales pitch of most other options out there are similar. That said, there are barriers, and some of them are big.

These barriers are shrinking, however -- and it’s possible for employers, no matter what their size, to offer these benefits to their Employees.

So what stops them from offering Earned Wage Access?

The biggest barrier for employees is that their employer doesn’t offer Earned Wage Access.

The biggest barrier for employers is having the ability to administer an Earned Wage Access program. For one, the actual dispersal of funds in regular pay cycles is generally done by way of a payroll provider who takes funds from the employer’s operating accounts and pushes funds to individual employee accounts. So employers don’t have an inherent in-house ability to make an ad-hoc advance on-the-fly. Those who do offer anything like this resort to paper checks, and those are an unnecessary administrative burden for the employers -- not to mention they don’t actually solve the need for the employee since most banks place a multi-day hold on checks. Because of this, we’ve seen an emergence of Earned Wage Access facilitators, like us, who deal with the movement of cash and make it possible for employers to offer an Earned Wage Access program.

However, even with Earned Wage Access service providers out there, activating a program for their employees comes with a lot of friction. These providers need to ensure they can check some basic boxes in order to get a service up and running for an employer:

- Data Exchange - EWA providers need historical employee payroll and time data to have certainty on employment status and hours worked

- Flow of Funds Out - Being able to seamlessly disperse early wages to employees, ideally without requiring employees to get a new card or bank account

- Flow of Funds Back - Being able to recover funds at time of paycheck, ideally without requiring a wholesale redirection of full payroll through your EWA provider

- Contracts - Setting up contracts with employers to ensure that their value is paid for

- Support - Answering questions from employees and still being able to go about running their business

The largest Earned Wage Access providers implement the service directly with their clients (big employers), which means they invest heavily in building data exchange mechanisms that allow them to not only read and understand the hours worked, timesheets punched, and wages accrued by individual employees but to be able to manage repayments and fees on upcoming paychecks. Often, they are also integrated right in the flow of funds as well -- in other words, employers have to direct all payroll through the Earned Wage Access provider, who then can disperse wages easily whether early or at paycheck time.

This can be a heavy lift for an employer, and these projects can take months, and usually involve major process changes as well. Large enterprises have systems that are geared for software integration and automatic exchange of data, and have internal teams who can not only implement the program technically, but teams that can oversee and support the program once it is up and running.

By contrast, in the mid-market, there are other challenges -- the systems with the required payroll and timesheet data are in a walled garden, often powered by software licensed by payroll service providers and PEOs, and offered to employers as a package. These software systems may have API or SFTP options available for data exchange, but mid-market employers do not generally have the internal resources to build and maintain an earned-wage-access service, and the cost of doing so is prohibitive with traditional Earned Wage Access providers.

Over the last 4 years, we’ve been very hard at work building ZayZoon for these mid-market companies. We have worked with key software systems so that employers can sign up and offer ZayZoon to their employees through their payroll providers with as little work as possible. We’ve found that employees don’t like to be told that they can only access their wages on-demand if they use a prepaid, debit or paycard that isn’t their own. While having a specific dispersal card is the only way some of our peers enable Earned Wage Access, we’ve been able to forego that through our partnership with VISA Direct, and give employees an option that works with their existing debit cards and bank accounts -- and still give them access to their wages nearly instantaneously. As an employer that works with one of our network payroll partners, activation is easy -- enabling Earned Wage Access for employees can literally happen in less than 60 minutes.

We are continuing to expand the network of HRIS platforms and payroll partners that connect with ZayZoon, so that more employers can activate the service for their employees. However, we also stopped and asked ourselves the big question: “What if we could make ZayZoon available to any business, so that any HR administrator, payroll administrator, or owner/operator could sign up and offer ZayZoon to their employees in the same 60 minutes, whether they had 10 or 10,000 employees?”

This question became a product goal. Delivering on this goal has been an incredible product design exercise -- full of technical challenges and user journey questions. I’m really excited about the progress we’ve made and continue to make as we structured the product offering and began to test it out with real businesses. We just completed our first alpha test of ZayZoon’s Employer Connect, and we’re very excited that we’re going to be the first true SAAS Wages On-Demand platform in the North American market. Our goal is to deliver a solution that is quick and easy to turn on, and does not require special internal resources or complex changes to business processes and workflows to make work.

The access that this will provide to employees in need, especially at a time like this, is the biggest favor employers can do for their employees, and for themselves and we’re pumped to enable more employers to take that step.

To offer Wages On-Demand to your staff, no matter how many you have and how big or small your company is, you can activate ZayZoon at zayzoon.com/employers.